Is the bad loan problem shifting to individuals from industries?

- Until the mid-2010s, banks used to lend massive loans to big industries. When these businesses failed, their loans turned sour. Such bad loans stayed hidden for sometime.

- In 2015, the Reserve Bank of India (RBI) carried out a review, following which skeletons tumbled out of the closet.

KEY HIGHLIGHTS

- The share of bad loans reached as high as 10% in 2017, which meant that nearly one in every 10 loans had turned bad.

- A variety of debt recovery channels including the Insolvency and Bankruptcy Code, 2016, were used to recover the money.

- Given the relatively high amount of loans lent to well-known companies, the failures to repay the loans were widely publicised.

- Following this debacle, banks started offering fewer loans to industries.

- They also managed to recover more and more bad loans.

- As a result, banks reached the pink of health in 2024.

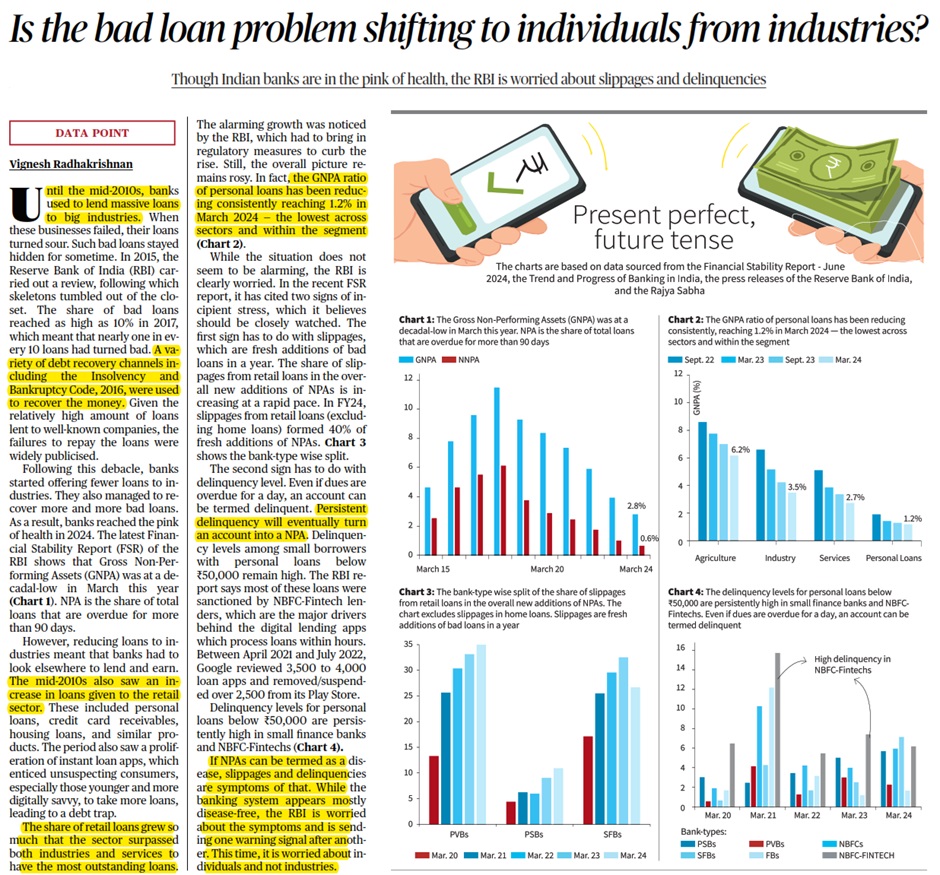

- The latest Financial Stability Report (FSR) of the RBI shows that Gross Non-Performing Assets (GNPA) was at a decadal-low in March this year .

- NPA is the share of total loans that are overdue for more than 90 days.

- However, reducing loans to industries meant that banks had to look elsewhere to lend and earn.

PERIOD OF MID 2010s

- The mid-2010s also saw an increase in loans given to the retail sector.

- The period also saw a proliferation of instant loan apps, which enticed unsuspecting consumers, especially those younger and more digitally savvy, to take more loans, leading to a debt trap.

- The share of retail loans grew so much that the sector surpassed both industries and services to have the most outstanding loans.

- The alarming growth was noticed by the RBI, which had to bring in regulatory measures to curb the rise.

- Still, the overall picture remains rosy.

- In fact, the GNPA ratio of personal loans has been reducing consistently reaching 1.2% in March 2024 — the lowest across sectors and within the segment (Chart 2).

- While the situation does not seem to be alarming, the RBI is clearly worried.

- In the recent FSR report, it has cited two signs of incipient stress, which it believes should be closely watched.

- The first sign has to do with slippages, which are fresh additions of bad loans in a year.

- The share of slippages from retail loans in the overall new additions of NPAs is increasing at a rapid pace.

- In FY24, slippages from retail loans (excluding home loans) formed 40% of fresh additions of NPAs.

- The second sign has to do with delinquency level.

- Between April 2021 and July 2022, Google reviewed 3,500 to 4,000 loan apps and removed/suspended over 2,500 from its Play Store.

- Delinquency levels for personal loans below ₹50,000 are persistently high in small finance banks and NBFC-Fintechs (Chart 4).

- If NPAs can be termed as a disease, slippages and delinquencies are symptoms of that.

- While the banking system appears mostly disease-free, the RBI is worried about the symptoms and is sending one warning signal after another.

- This time, it is worried about individuals and not industries.